Inside the article

Request a product demo

Get a demo and clarify your doubts about our software.

Key Takeaways

- Taxi insurance in the U.S. is pricier than personal auto insurance because of commercial use and passenger liability.

- Monthly premiums vary from approximately $560 in low-risk states to over $1,200 in high-risk states like New York.

- Operators usually require high liability coverage of around $1M CSL, affecting costs.

- Factors such as driver history, vehicle type, and coverage limits lead to significant price variations.

- Telematics and AI software can help reduce risk and lower premiums over time.

Taxi cab insurance is a necessary cost for legally running a taxi business in the United States. Because taxis operate for commercial purposes and transport passengers every day, the insurance costs are higher than those for personal auto insurance.

This guide covers average taxi insurance costs, pricing by state, available coverage types, and tips for lowering premiums, and helps you budget properly and stay compliant in 2026.

How much does taxi insurance cost?

Taxi cab insurance is generally more expensive than regular car insurance because it covers commercial use, passenger liability, and higher driving risks.

Costs vary based on factors like location, coverage limits, driving history, and service demand, but you can refer to general averages for planning.

Average monthly premium

On average, taxi insurance costs $952 per month per vehicle.

Small operators in low-risk areas may pay closer to the lower end, while taxis operating full-time in busy urban areas usually pay more due to higher accident and claim risks.

Average annual premium

Annually, taxi insurance typically ranges between $4,800 and $9,600 per vehicle.

This amount increases if you need higher liability limits, uninsured motorist coverage, or additional protection for multiple drivers and shifts, which covers taxi driver insurance costs.

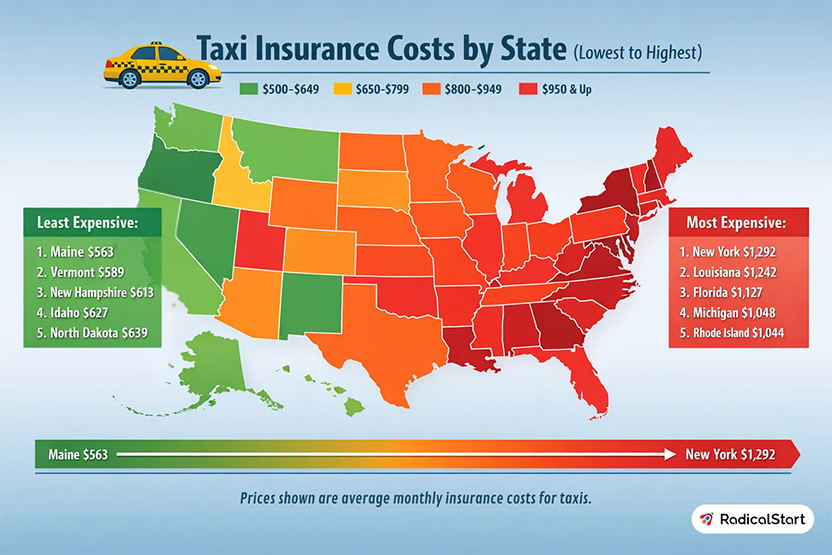

Cost by state (lowest to highest)

According to MoneyGeek, the following figures represent the average cost for taxi cab insurance, monthly taxi insurance costs by state, arranged from lowest to highest.

Taxi insurance costs vary significantly by state due to traffic density, claim frequency, and local insurance regulations.

- 1. Maine - $563

- 2. Vermont - $589

- 3. New Hampshire - $613

- 4. Idaho - $627

- 5. North Dakota - $639

- 6. Iowa - $665

- 7. Hawaii - $668

- 8. Utah - $695

- 9. Alabama - $707

- 10. Nebraska - $707

- 11. Montana - $711

- 12. Wyoming - $721

- 13. Wisconsin - $730

- 14. North Carolina - $737

- 15. Oklahoma - $749

- 16. Arkansas - $765

- 17. Mississippi - $765

- 18. Ohio - $775

- 19. Indiana - $776

- 20. West Virginia - $786

- 21. Georgia - $789

- 22. South Carolina - $794

- 23. New Mexico - $806

- 24. Kentucky - $817

- 25. Alaska - $846

- 26. Oregon - $848

- 27. Virginia - $849

- 28. Tennessee - $854

- 29. Delaware - $860

- 30. Minnesota - $889

- 31. Arizona - $890

- 32. Pennsylvania - $899

- 33. South Dakota - $902

- 34. Nevada - $907

- 35. Missouri - $948

- 36. Texas - $973

- 37. Illinois - $974

- 38. Colorado - $977

- 39. Washington - $1,000

- 40. New Jersey - $1,005

- 41. Connecticut - $1,011

- 42. Massachusetts - $1,018

- 43. California - $1,019

- 44. Maryland - $1,020

- 45. Rhode Island - $1,044

- 46. Michigan - $1,048

- 47. Florida - $1,127

- 48. Louisiana - $1,242

- 49. New York - $1,292

This difference in pricing highlights why the location is more influential on taxi insurance costs than the vehicle itself.

Factors that influence your taxi insurance cost

Insurers look at a mix of risk signals tied to where you operate, how your business runs, and who’s behind the wheel. Here’s what matters most.

Location

High-traffic cities with frequent accidents, theft, and lawsuits generally result in higher premiums.

In contrast, rural and low-density areas typically cost less due to fewer claims and lower repair expenses.

Type of taxi business

Full-time city taxis, airport taxis, and fleet-based operations usually cost more than part-time or pre-booked services.

Higher daily mileage and constant passenger turnover increase exposure for insurers.

Type of vehicle

Vehicle value, repair costs, and safety features all play a role. Luxury sedans, SUVs, and newer models cost more to insure, while older or standard vehicles with good safety ratings tend to be cheaper.

Hybrid and electric vehicles may also affect pricing due to repair complexity.

Driver age and driving history

Younger drivers or drivers with past accidents, tickets, or claims typically face higher taxi driver insurance costs.

Experienced drivers with clean driving records are considered lower risk and are rewarded with better rates.

Coverage amount

Higher liability limits and add-ons like comprehensive, collision, uninsured motorist coverage, or medical payments increase insurance costs.

Choosing only the minimum required coverage lowers premiums but also reduces protection.

These factors explain why similar taxis can have very different insurance costs based on their operation and location.

Types of taxi insurance coverage explained

Taxi insurance includes several types of coverage that protect drivers, passengers, vehicles, and the business itself.

Here are the most common types of coverage, along with typical monthly cost ranges.

Note: The cost may vary depending on the city or location.

Primary liability insurance

This is the core and legally required coverage for taxi operations. It protects you when your taxi causes injury or damage to others.

In the commercial sector, you pay one premium for Liability, which is then structured as either a CSL or a Split Limit.

Combined Single Limit (CSL)

Combined Single Limit (CSL) is a type of taxi liability insurance that provides one coverage amount for both bodily injury and property damage per accident.

In the U.S., most taxi operations need a standard CSL of $1 million. Some smaller towns accept $300,000, while larger areas often require $2 million or more.

CSL streamlines the claims process and is widely accepted by regulators.

Although higher CSL limits can lead to higher premiums, they offer better protection and help with compliance.

Average Cost: $350 to $750 per month.

Split Limit

Split limit liability insurance divides coverage into separate limits for bodily injury and property damage instead of offering one combined amount.

This type of coverage is less flexible than combined single limit (CSL) insurance, and many cities and airports in the U.S. do not accept it. However, some small-town or private taxi operators may still use it if it is allowed.

Bodily injury coverage

This coverage includes medical expenses, legal fees, and settlements for injuries to passengers, pedestrians, or other drivers caused by your taxi.

Average costs range from $400 to $800 per month for split-limit liability, depending on the per-person and per-accident limits (e.g., 100/300).

Property damage coverage

This insurance covers repair or replacement costs for another person’s vehicle or property damaged in an accident where your taxi is at fault.

The average cost is included in the primary liability premium, which ranges from $400 to $800 per month, with higher coverage limits potentially increasing the cost.

Important Note:

Under split limits, bodily injury and property damage coverage are combined into a single liability policy, rather than being priced separately.

Although split limits may be slightly cheaper than Combined Single Limits (CSL), they provide less flexibility in payouts.

General liability

General liability covers non-driving-related incidents. This includes passenger slip-and-fall injuries, damage to customer property, or injuries that occur while entering or exiting the taxi.

It’s especially important for taxi companies with offices, dispatch centers, or multiple vehicles.

Average cost: $50 to $150 per month.

Physical damage coverage

This coverage protects your taxi vehicle itself from damage, regardless of fault.

Comprehensive coverage

Covers non-collision events such as theft, vandalism, fire, floods, falling objects, or weather-related damage. It’s essential in areas prone to extreme weather or high theft rates.

Average cost: $50 to $120 per month.

Collision coverage

Pays for repairs or replacement of your taxi if it’s damaged in a collision with another vehicle or object, even if the accident is your fault.

Average cost: $90 to $250 per month.

Medical payments coverage

Helps cover medical expenses for the driver and passengers after an accident, regardless of who caused it.

This can include hospital visits, ambulance fees, and immediate treatment costs.

Average cost: $60 to $150 per month.

Workers’ compensation

Required if you employ drivers. Workers’ compensation covers medical bills and lost wages if a driver is injured while working.

It also protects the business from employee injury-related lawsuits.

Average cost: $100 to $300 per driver per month, depending on state laws and payroll.

Together, these coverages form a safety net that keeps your taxi business compliant, protected, and financially stable when unexpected events occur.

Taxi insurance vs ride-hailing insurance

While both taxi and ride-hailing insurance cover vehicles used for paid passenger transport, they are structured very differently. The differences matter for compliance, cost, and how claims are handled.

Taxi insurance

Taxi insurance is a complete commercial auto policy meant for vehicles that transport passengers all day. Coverage is active at all times, whether the driver is waiting for passengers or is on a trip.

It typically includes high liability limits, often $1M CSL or more. It may also require general liability and is often required by city or airport authorities.

Premiums are higher because the risk exposure is always present.

Ride-hailing insurance

Ride-hailing insurance focuses on app-based driving for services like Uber or Lyft. Coverage varies based on the driver’s status: offline, waiting for a ride, or carrying a passenger.

Most ride-hailing companies offer limited commercial coverage during active trips. Drivers often depend on personal or hybrid policies when they are not active.

Insurance costs are usually lower than those for taxi services, but they rely heavily on how frequently the driver is online.

👉 Know more about how to start an online taxi business.

Coverage

Taxi insurance offers continuous commercial coverage and higher limits because it is regulated.

Ride-hailing insurance provides coverage based on specific periods and involves a mix of personal and commercial policies.

For claims handling, taxi claims go through one insurer, while ride-hailing claims may involve both the platform and the driver’s insurer.

In short, taxi insurance is meant for full-time passenger transport, whereas ride-hailing insurance is designed for part-time, app-based driving.

How technology can lower your taxi insurance costs

Insurance pricing is driven by risk data. The more insight insurers gain into how safely and efficiently your taxis run, the more likely they are to lower premiums.

Modern taxi technology not only makes operations better, but it also reduces insurable risk.

Real-time driver monitoring

Telematics and in-vehicle monitoring systems track speed, braking, acceleration, idle time, and driving hours.

When insurers see consistent safe-driving behavior, fewer violations, and lower accident probability, they often offer lower premiums or renewal discounts.

It also helps operators correct risky driving patterns before they turn into claims.

Route optimization

Smart route optimization cuts down on unnecessary mileage, limits exposure to congested areas, and avoids accident-prone roads.

Driving fewer miles in high-risk zones leads to a lower frequency of accidents, which insurers consider when setting prices.

Efficient routing also shortens trip times, which helps reduce driver fatigue; this is another significant risk factor.

AI-powered taxi software

AI-powered taxi software combines driver data, trip history, vehicle maintenance, and smart dispatch into one system. Predictive maintenance reduces breakdown-related accidents, while AI-based dispatch prevents driver overwork.

We, at RadicalStart, provide an AI-powered taxi booking software that uses AI to translate languages in real time, reducing misunderstandings and disputes.

Insurers see fewer accidents, fewer complaints, and cleaner risk data, which directly supports lower insurance premiums.

Top 3 budget taxi insurance providers in the USA

Here’s a look at three of the most affordable and popular commercial taxi insurance providers for taxi businesses in the United States, based on nationwide rate comparisons and industry data.

ERGO NEXT

ERGO NEXT is often considered the affordable taxi insurance provider.

It offers competitive rates for commercial taxi liability and physical damage coverage. Many small business owners appreciate its digital-first platform and fast online quoting process, which helps keep costs down.

The national average cost for taxi cab insurance, monthly premiums with ERGO NEXT are some of the lowest in the industry.

Typical premium:

- $910 per month Best for: Solo drivers and small taxi businesses focused on affordability.

The Hartford

Hartford is recognized for its strong customer service and reliable coverage options. It consistently ranks high in customer experience and offers customized commercial auto policies, including taxi insurance.

Its combination of price and service makes it a preferred choice for small fleets and owner-operators.

Typical premium:

- $983 per month Best for: Small to mid-size fleets needing stable coverage and good claims handling.

Nationwide

Nationwide provides reliable commercial taxi insurance with good bundling options and wide coverage. Its rates are a bit higher than those of ERGO NEXT and The Hartford on average.

However, Nationwide's network and support services offer strong value for taxis seeking complete protection and flexibility.

Typical premium:

- $1,011 per month Best for: Growing fleets and taxis operating across multiple cities or states.

Conclusion

Taxi cab insurance costs in the U.S. vary widely based on location, coverage limits, vehicle type, and how the business operates.

Monthly premiums usually range from $400 to over $1,200. Choosing the right coverage, using technology to lower risk, and comparing affordable insurers can help reduce costs.

The key is to balance compliance, protection, and affordability to keep your taxi business insured and profitable.

Request a product demo

Get a demo and clarify your doubts about our software.